ジャンプリンクテキスト

On May 18, 2021, the International Energy Agency (IEA)—the world’s leading energy policy intergovernmental organization—released a comprehensive report, “Net Zero by 2050: A Roadmap for the Global Energy Sector” (Report). The Report outlines the IEA’s view of the steps that must be taken globally in order to meet the goal of “net zero” global greenhouse gas emissions by 2050, which is in turn required to meet countries’ commitments under the Paris Agreement to limit global warming to 1.5°C.[1] The Report is the first of its kind focused on the global transition to net zero emissions, whilst purporting to safeguard stable and affordable energy supplies and supporting strong economic growth.[2]

Companies are currently challenged by the cost of implementing clean energy into their current business models and portfolios in a manner that will generate attractive investment returns. In addition, the scale of new clean energy sources that would be needed to fully replace fossil fuel powered sources is so great that some element of fossil fuel-powered sources will still be necessary in the 2050 scenario.[3] For these reasons, the world remains predominantly reliant on fossil-based energy such as oil and natural gas. The Report confronts this roadblock by outlining cost-effective pathways to achieve a clean, dynamic energy economy underpinned by renewables and clean energy technologies.[4]

The Report calls for a complete transformation of the energy economy comprising more than 400 milestones, including innovation, policy design and implementation, technology deployment, infrastructure building and ambitious investment targets totaling trillions of dollars (approximately $90 billion of public money is needed for demonstration projects before 2030).[5] Importantly, the IEA stresses that this extremely challenging path forward requires contributions by all key stakeholders, including governments, businesses and investors.[6]

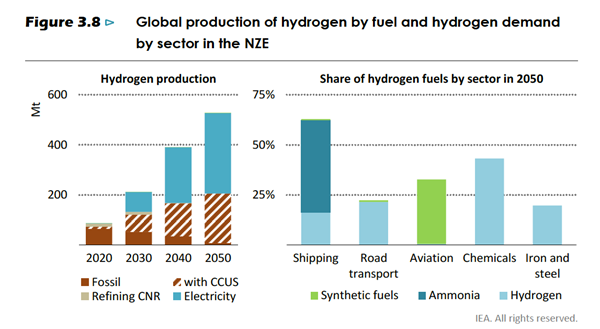

So, where does hydrogen fit into the overall net zero strategy? The Report singles out hydrogen electrolyzers—the technology for combining electricity and water to obtain hydrogen—as one of the biggest energy innovation opportunities, together with advanced batteries and direct air capture and storage (CCUS) of greenhouse gases. The Report notes that, whereas hydrogen use in today’s energy economy is currently limited to “dirty” processes associated with oil refining and the production of ammonia and methanol for decarbonization targets to be met, hydrogen is expected to meet 13 percent of total global energy demand by 2050 and two crucial drivers must emerge—demand for hydrogen in industry and transportation sectors must increase exponentially and the production route for hydrogen must change to cleaner technology.[7] The IEA envisions a future where hydrogen production is based on low‐carbon technologies, including water electrolysis making up 60 percent of global production, and the remainder coming from conversion of natural gas with CCUS.[8]

|

The choice between electrolyzers and natural gas plus CCUS will be driven by economic factors, specifically (on the supply side) increasing the cost of natural gas and reducing the availability and cost of electricity, and other factors such as the geographic proximity to renewable energy and the viability of carbon storage.[9]

The Report focuses in on the important role that electricity plays in hydrogen’s story: both as part of the production process but also, in light of its capacity to convert excess electricity into a chemical carrier for future conversion back to electricity, as a way to help balance seasonal fluctuations in renewable electricity demand and imbalances.[10] In addition, the IEA believes that, through retrofitting gas-fired plants to co-fire with hydrogen as well as retrofitting coal-fired power plants to co-fire with ammonia, hydrogen and hydrogen‐based fuels represent a low‐carbon source that provides flexibility to the electricity system.[11]

The IEA predicts that by 2050 the production costs for hydrogen from natural gas with CCUS will be around $1–2 per kilogram (kg) of hydrogen, with gas accounting for 15–55 percent of total production costs, while water electrolysis production should see capital expenditure reductions of 60 percent by 2030 due to learning effects and economies of scale.[12] Lowering the cost of low-carbon electricity will ultimately determine the reductions in production costs since electricity is currently responsible for 50–85 percent of total hydrogen production costs. The Report anticipates the average cost of producing hydrogen via electrolysis with renewable electricity will decrease from $3.5–7.5/kg today to approximately $1.5–3.5/kg in 2030 and $1–2.5/kg in 2050 (in concurrence with other recent high-profile analyses that see this so-called “green hydrogen” becoming price-competitive with the “blue hydrogen” produced from natural gas with CCUS).[13] Further, the IEA emphasizes the criticality of increasing the annual investment in carbon capture pipelines and hydrogen enabling infrastructure from $1 billion today to around $40 billion in 2030.[14]

Government involvement is critical to support the transition to net zero, and the Report encourages governments to immediately begin assessing the opportunities and challenges of developing a low‐carbon hydrogen industry as part of national strategy. Domestic policy should in its view specifically encompass the potential production of hydrogen from renewable electricity via water electrolysis or from gas with CCUS, or importation of hydrogen-based fuels.[15] In addition to developing and implementing a strategy, governments should establish methodologies to determine the carbon footprint of production routes in order to facilitate hydrogen trade. Governments should also focus on international cooperation to harmonize safety standards and regulations on hydrogen concentration in gas grids, which would aid increased production and cost reductions related to blending hydrogen into existing gas networks.[16]

The major infrastructure required for low-carbon hydrogen to succeed, including repurposing existing gas pipelines and connecting those pipelines to large hydrogen demand hubs, will require governments to facilitate planning with stakeholders. Governments will also likely need to encourage direct public investment or public‐private partnerships and share some of the investments risks for large projects.[17]

Reaction to the Report has run the gamut: ranging from excitement and hope for a net zero future from the largest privately-owned renewable energy group, to pragmatism from the U.S.’ largest industry group which stated that the required technology is not yet invented and oil and gas are still essential to the enablement of renewable energy.[18] Though the Report is receiving mixed reactions from more traditional oil and gas companies, the Report does offer an important contribution to developing a business strategy that accounts for a decrease in reliance on fossil fuels.[19]

[1] International Energy Agency, “Net Zero by 2050: A Roadmap for the Global Energy Sector,” May 2021.

[3] International Energy Agency, “Net Zero by 2050: A Roadmap for the Global Energy Sector,” May 2021.

[5] International Energy Agency, “Net Zero by 2050: A Roadmap for the Global Energy Sector,” May 2021.

[6] Id

[7] Id

[8] Id

[9] Id

[10] Id

[11] Id

[12] Id

[13] Id

[14] Id

[15] Id

[16] Id

[17] Id

[19] Id.