June 14, 2018

Jump to...

On June 12, 2018, following a six-week-long bench trial, Judge Richard J. Leon of the United States District Court for the District of Columbia ruled that AT&T’s proposed acquisition of Time Warner does not violate the antitrust laws, rejecting the United States Department of Justice’s (DOJ) challenge to the merger. This case—the first vertical merger challenge tried by the Justice Department since 1977—demonstrates the difficulty in challenging mergers where a competitor is not eliminated by the transaction.

On October 22, 2016, AT&T announced that it had reached an agreement with Time Warner under which AT&T would acquire Time Warner in a stock-and-cash transaction with a total equity value of $85.4 billion. AT&T is the world’s largest telecommunications company and the country’s second-largest wireless telephone company. AT&T also owns DirecTV, the nation’s largest distributor of traditional subscription television. Time Warner owns HBO and Turner Broadcasting System, which includes many of the country’s top television networks, such as TNT, TBS and CNN.

Section 7 of the Clayton Act prohibits mergers and acquisitions where the effect of the transaction “may be substantially to lessen competition, or to tend to create a monopoly.” A vertical transaction is one that is between two firms that operate at different levels of the value chain. There are three theories of how a vertical merger can violate Section 7.

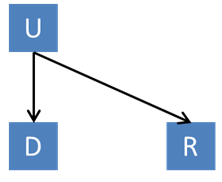

Foreclosure. Firm U (the upstream firm) and Firm D (the downstream firm) combine. If U produces a critical input for D and D’s rival R, then the combined U-D can refuse to sell U’s product to R, cutting R off from the critical input and driving R out of business. This is the classical theory of vertical harm.

Raising rivals’ costs (RRC). This is a weakened version of the foreclosure theory. U now produces an important input for the downstream firms. Rather than U-D cutting off R, U-D simply raises the price to R. Now, some of the customers R loses will “divert” to D. Before the merger, U earns nothing from the diversion, but after the merger, U “recaptures” some of its lost profits from the price increases. This is the modern theory on which most vertical merger challenges are grounded and the DOJ’s primary theory of anticompetitive harm in the AT&T/Time Warner case. Note that if U cannot refuse to deal with R, then U cannot “hold out” and prices should not change postmerger. For this reason, the agencies have traditionally resolved vertical concerns through behavioral relief solutions that require mandatory dealing.

Anticompetitive information conduits. Premerger, U knows competitively valuable information through its dealings with R. After the merger, U can share this information with D to competitively advantage D and disadvantage R. Historically, the agencies have accepted behavioral consent decree relief, imposing information firewalls on U so that it cannot share competitively sensitive information with D.

Although AT&T was willing to accept behavioral restrictions in the form of an arbitration commitment, which the DOJ in the Obama administration had accepted in Comcast/NBCUniversal—a similar transaction—here, the DOJ rejected behavioral relief as inadequate to ensure effective competition remained postmerger. When the merging parties declined to accept a divestiture solution to resolve the DOJ’s vertical concerns, the DOJ brought suit to enjoin the merger.

On November 20, 2017, the DOJ filed a lawsuit to block the proposed merger, alleging that it would harm consumers under the RRC theory by giving the combined firm increased bargaining leverage such that it could raise prices to AT&T’s rival traditional video distributors. The DOJ also alleged that the merger would give the combined firm the incentive and ability to impede entry and growth of disruptive online video distributors through unilateral conduct and tacit coordination, and restrict or foreclose rival distributors’ access to using HBO as a promotional tool. In this note, we will focus only on the RRC theory, as it was the focus of the government’s case-in-chief.

The government’s primary theory of harm, and that which occupied much of the six-week trial and the bulk of the court’s opinion, was that the merged firm would be likely to raise the prices of “must-have” Time Warner content to the distribution rivals of AT&T, which in turn would raise prices to their customers. If, as the DOJ theorized, the merged firm threatened to withhold “must-have” programming such as live sports and 24-hour news programming from rival distributors (without which, they argued, distributors cannot compete), the merged firm could demand higher prices and more favorable terms from its competitors. The government argued that Turner’s bargaining leverage would increase as a result of its relationship with AT&T because the combined firm would not face the unmitigated downside of losing affiliate fees and advertising revenues if it blacked out a distributor. Rather, it could recapture some profits because some portion of customers lost by the rival distributor would switch to AT&T. This added downside protection, the government argued, would make the blackout threat more credible and allow the combined firm to extract higher prices for its content in affiliate fee negotiations.

The defendants argued that the proposed merger is necessary to compete effectively for advertising revenues with competitors such as Amazon, Netflix, Hulu and Google, each of which can use consumer data to target and tailor digital advertisements. These “tectonic changes” in the industry, defendants argued, result in declining subscriptions and flatlining advertising revenues for programmers like Time Warner and distributors like AT&T—a problem which they argued would be solved by combining Time Warner’s programming and advertising offerings with AT&T’s customer relationships and valuable data about programming. Moreover, defendants argued that a long-term blackout of Turner content, even postmerger, would cause Turner to lose more in affiliate fees and advertising revenues than the merged entity would be able to recapture. Finally, defendants argued that the government’s evidence was insufficient to predicate their bargaining model and was rife with methodological flaws.

Framework

Judge Leon began his formal analysis with some basics of vertical merger law. He recognized that vertical mergers can have both procompetitive and anticompetitive effects and that they can violate Section 7 only when the anticompetitive effects of the merger outweigh the procompetitive effects. In other words, he concluded that vertical mergers are not per se legal.

Next, Judge Leon held that the three-step burden shifting approach that Baker Hughes[1] had applied to horizontal mergers applies equally to vertical mergers. Under Baker Hughes, the plaintiff bears the burden of proving a prima facie case of anticompetitive effect—that is, that the merger is likely to substantially lessen competition in the absence of any offsetting procompetitive benefits. If the plaintiff makes out its prima facie case, the burden of going forward with evidence shifts to the merging parties to prove some offsetting procompetitive effect. If the merging parties make their showing, then the burden of persuasion returns to plaintiff to prove that, in light of all of the evidence, it is reasonably probable that the merger will have an anticompetitive effect in the relevant market.

The court noted that the plaintiff’s proof of prima facie anticompetitive effects under the first step of Baker Hughes is typically more difficult in vertical cases than in horizontal cases. In horizontal cases, plaintiffs can avail themselves of the Philadelphia National Bank[2] presumption, which holds that if the merger results in a firm with an “undue market share” and a “significant increase” in market concentration, the merger is presumed to be anticompetitive. Judge Leon observed that there is no corresponding presumption in vertical cases, so the plaintiff will have to prove its prima facie case entirely on affirmative evidence. Moreover, although market definition is often a critical issue in horizontal cases—because market shares are often sensitive to the precise market boundaries—market definition is much less important in vertical cases since outcomes do not turn on shares. As a result, although market definition remains an element of a Section 7 case on which the plaintiff bears the burden of proof, Judge Leon accepted the DOJ’s alleged market definitions without particularly deep analysis.

Turning to the DOJ’s theory of anticompetitive harm, Judge Leon accepted the government’s RRC/bargaining model as an appropriate framework for analysis and one that was not theoretically unsound. In order to prove a prima facie case of anticompetitive effect under the first step in Baker Hughes, the DOJ had to prove facts that, when the model was applied, demonstrated an anticompetitive effect in the form of higher prices for Time Warner content to AT&T’s rivals. But a simple showing that prices would increase was not enough. Judge Leon required that the DOJ show that the price increases would overcome three hurdles.

First, the evidence, when applied to the RCC/bargaining model, had to show a price increase to AT&T’s rivals.

Second, a well-accepted benefit of vertical integration is the elimination of double marginalization. Judge Leon’s second hurdle was that the DOJ had to show that the price increases to the customers of AT&T’s rivals under the RRC/bargaining model were greater than the price decreases to AT&T’s customers resulting from the elimination of double marginalization. Significantly, the lead expert witness conceded that the merger would result in savings of $352 million annually through elimination of double marginalization, so that the DOJ started off from a position of disadvantage in showing an anticompetitive price increase.

Finally, Judge Leon required that the DOJ show that the price increases were sufficiently higher than the price decreases to qualify as a substantial lessening of competition. This is different than the usual agency view that any non-justified price increase resulting from a merger makes the merger anticompetitive.

The DOJ’s Evidence

To prove its prima facie case, the DOJ relied primarily on two types of evidence: lay testimony from AT&T’s distributor rivals that the prices they pay for Turner content would increase, and expert testimony based on an economic model by Professor Carl Shapiro of the University of California, Berkeley, who previously served as the DOJ’s chief antitrust economist. Professor Shapiro presented a model that forecast an initial $436 million per year pay-TV rate increase for consumers in a postmerger world (escalating to $571 million by 2021). He projected that pay-TV distributors would have to stomach an even higher price increase, but the $436 million reflected the amount that would be passed down to consumers. The court ultimately rejected both types of evidence as insufficient to establish a prima facie case of any price increase.

The court found that the third-party testimony, although heartfelt and sincere, could not be credited. When pressed, Judge Leon found, the witnesses could not explain the mechanism by which Time Warner’s bargaining power would increase against them postmerger or provide a basis for concluding that they would lose a significant percentage of their customers should they lose the Time Warner content. Thus, Judge Leon did not find their testimony to be probative of a likely price increase.

The court likewise rejected the government’s expert testimony as insufficient to establish a price increase. First, Judge Leon was persuaded by defendants’ evidence that the DOJ was overstating the importance of Time Warner content to distributors and the corresponding bargaining leverage that the Turner Broadcasting programming portfolio affords. Defendants had argued that “must-have content” is simply a marketing term used by virtually every programmer and does not imply that the content is “literally ‘must have’ in the sense that distributors cannot effectively compete without it.”[3] While a distributor might lose customers if it did not have Turner content, it would not necessarily fail financially.

This makes the number of customers that would be lost if the content were withdrawn critical to the analysis. To determine that number, Professor Shapiro posited a permanent blackout as a threat in the bargaining game. But, based on trial testimony the court rejected that threat as not credible, which qualitatively undermined the DOJ’s argument that the merger would increase the combined firm’s bargaining leverage.

Moreover, Judge Leon rejected several of the essential numerical predicates that Professor Shapiro used in his model. In particular, Judge Leon found that the percentage of customers that rivals would lose if there was a blackout of Turner content was significantly overstated. As a result, the model significantly overestimated the “recapture” of profits the combined firm would earn as customers from disadvantaged rivals diverted to AT&T.

Finally, Judge Leon was persuaded by defendants’ numerous methodological attacks on Professor Shapiro’s model. The defendants presented their own expert witness—Professor Dennis W. Carlton of the University of Chicago, who is himself a former DOJ chief antitrust economist. Professor Carlton labelled Professor Shapiro’s economic model “theoretically unsound,” arguing that it ignored key variables and had questionable data inputs. For example, Professor Shapiro calculated the lifetime value of pay-TV customers based on AT&T’s June 2016 estimates, which were 40% higher than the newer June 2017 estimates relied on by Professor Carlton.

Efficiencies and “Litigating the Fix”

Having found that the DOJ’s evidence was insufficient to make a prima facie showing of any price increase, the court concluded that the DOJ had failed to satisfy the first step of the Baker Hughes test. This had two important implications.

First, apart from the benefits resulting from the elimination of double marginalization, procompetitive benefits did not play a role in the formal analysis. Although the court observed that efficiencies in addition to elimination of double marginalization from the transaction were large and credible, the formal analysis did not require any other efficiencies because the burden never shifted away from the government.

Second, the arbitration commitments made by the defendants also did not play a role in the formal analysis. AT&T made this commitment in order to deprive the government of the argument that Time Warner could refuse to license content (a strategy known as “litigating the fix”). Although Judge Leon acknowledged the commitments and found that they would be continued by the merged company with an effect on bargaining, he did not expressly rely on them in his competitive analysis.

This is not to say that the efficiencies and arbitration commitment had no effect on the outcome of the case. Certainly, these two factors must have given Judge Leon greater confidence in the correctness of his decision. But they did not play a role in the formal reasoning leading to the court’s conclusion that the DOJ did not meet its burden of proving an anticompetitive effect.

After denying the government’s request to enjoin the merger, Judge Leon cautioned the government against seeking a stay of his order pending appeal to the Court of Appeals. Such a stay, he stated, would cause irreparable harm to the defendants by preventing closing from occurring prior to the June 21, 2018 outside date under the merger agreement. Based on this, Judge Leon concluded that a stay pending appeal would be a manifestly unjust outcome.

The District Court’s decision in United States v. AT&T highlights a number of important considerations that parties contemplating a transaction should keep in mind, including the following:

[1] United States v. Baker Hughes Inc., 908 F.2d 981 (D.C. Cir. 1990).

[2] United States v. Philadelphia Nat'l Bank, 374 U.S. 321 (1963).

[3] Memorandum Opinion at 77 United States v. AT&T Inc., No. 1:17-cv-02511 (D.D.C. filed Jun. 12, 2018).