Jump to...

“Probable impossibilities are to be preferred to improbable possibilities.”

–Aristotle

SOFR – the secured overnight funding rate in USD – is a rate published by the New York federal reserve based upon secured overnight transactions in the repo market. It is of increasing importance, since it has been regarded by many market participants as the basis for the likely successor to U.S. dollar LIBOR, a long-standing benchmark which is being phased out at the behest of the UK’s Financial Conduct Authority.

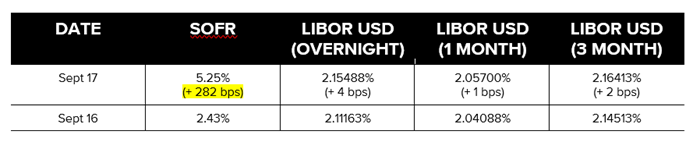

The confluence of a number of events has exposed insufficient elasticity in the USD overnight cash repo market. Contributing to the stress on the system is an upcoming corporate tax payment date, which pulled cash out of the money market system, whilst at around the same time $115 billion of investment grade debt was being issued and traded (based on data for the first half of September). The secondary market trading volumes of this newly issued investment-grade paper increased inventories at broker dealers; who, in turn, rely on the repo market to fund those volumes. In addition, $60 billion of Treasury bond maturities negatively impacted available cash. All these events contributed to a cash crunch on September 17, 2019, that we refer to here as the “SOFR Surge Event”, in which the SOFR rate increased by 282 basis points, compared with the previous day. As of the time of this publication, the surge is not expected to last more than one day (albeit an uptick in SOFR may temporarily linger, given its causes (which are of a temporary nature)).

Backward-looking cumulative 1 month SOFR has been discussed as a new USD rate benchmark for the derivatives markets to replace the floating rate for forward looking 1 month USD LIBOR. Since this is based upon actual SOFR overnight rate data, this rate will continue to capture and incorporate the effects of the SOFR Surge Event for the next month. Given the 282 basis points of surge and assuming this is very short-lived (i.e., the event lasts one day), the increase to the 1-month SOFR for each of the 30 days following the SOFR Surge Event will be approximately 10 basis points. This is not just material in the world of interest rate pricing, but of huge economic impact. For those who are interest rate traders, this SOFR Surge Event presents a material change for risk management purposes and complicates managing a complex book of interest rate positions. The risk of future such events will also need to be taken into account by banks when agreeing on rates with their counterparties.

In contrast to backward-looking SOFR, LIBOR is forward looking. For example, the 1 month USD LIBOR setting would take account of changes that LIBOR submitting banks foresee in the month ahead. So the 1 month rate would include the average effect of any expected month end uplifts to interest rates. Unexpected/flash events that are anomalous and very short lived would not usually be factored into LIBOR, because forward expectations should exclude unexpected and (with significant exceptions) also exclude historical outcomes. This is an important stabilizing component of LIBOR that is often overlooked, but is underscored by this recent SOFR Surge Event.

There are some interesting implications.

First, in relation to the proposed transition from LIBOR to fallback or alternative rates (meaning, in the USD market, SOFR-based rates). The proposal at the moment, which has wide market support, is ultimately for a SOFR-based rate (likely a cumulative overnight backward-looking rate, as described above) plus a fixed spread, to replace the relevant LIBOR rate setting. The fixed spread would be determined as the average difference between SOFR and LIBOR over a historic period. If the transition date had, for example, been declared and set to be the end of September 2019, the fixed spread as between SOFR and LIBOR would be calculated over a period including the SOFR Surge Event and the entire USD LIBOR floating rate market would suffer an artificially increased fixed spread as a result. An excess 10bps (if the fixed rate averaging period is a month) rippling across trillions of dollars of assets and liabilities is a matter of grave concern and potentially has systemic implications.

Secondly, in relation to the robustness of the SOFR rate itself, the SOFR Surge Event raises the troubling reminder that the cash market stabilization role played by the repo market, through the Fed lending window, is ultimately managed through discretionary mechanisms controlled by the Fed. In this instance, the Fed, briefly, was unable to intervene to stabilize the overnight rate, with the result that there was a surge in the SOFR rate. The corollary is that SOFR is, in large measure, determined from input data that is dependent on Fed activity and the ability and effectiveness of the Fed’s market stabilization activity, and that SOFR may be affected by one-off economic events and greater levels of volatility than have been observed with LIBOR. It is therefore questionable whether SOFR can be truly characterized as a market rate or is yet suitable to be used on a market-wide basis. It is a government-managed rate that is subject to discretionary adjustment by the Fed. The argument that a replacement rate (for LIBOR) should be based in transparent actual transactions is still valid. SOFR was calculated in accordance with its published formula based on actual transactions. However, its utility as a market replacement rate is weaker than expected. In contrast, the USD LIBOR market was stable during the occurrence of the SOFR Surge Event. The broader cash market was also stable. It is hard to balance the cash market stabilization role played by the Fed through the overnight repo market with the goal of creating a market replacement rate. Suffice to say that any equivalent discretion afforded to a non-government agency would instantly disqualify the resulting rate from being sufficiently robust and not subject to manipulation or unanticipated external shocks.

Thirdly, the SOFR Surge Event not being reflected in LIBOR outputs on September 17 shows that SOFR is “almost, but not entirely, unlike”[1] LIBOR. The transactions which qualify as inputs for LIBOR settings are not the same as those that underpin SOFR. The former are unsecured, while the latter are secured; LIBOR is forward-looking, whilst SOFR is backward-looking. The ripple effect of the SOFR Surge Event on LIBOR qualifying transactions is not clear, but we can infer (given the apparent stability of LIBOR) that (1) the SOFR Surge Event was possibly too short in duration to impact interbank lending (i.e., a “flash” event), (2) a significant number of LIBOR submitting banks were not meaningfully exposed to the SOFR Surge Event and therefore were able to continue orderly interbank lending or (3) given the forward looking nature of LIBOR, the LIBOR submitting banks determined that the SOFR Surge Event was anomalous and one-off and therefore not relevant to the forward-looking LIBOR market.

As transitions from LIBOR to other rates are rolled out by financial institutions to their contracts, such as derivatives, lending agreements, mortgages, securities and so on, it will be necessary for them to explain what the change to customers will be from the new rates. As a practical matter, it will likely be an incrementally harder sell to customers to disclose that changing the rate to SOFR will expose customers to the risk of more extreme volatility and off-market pricing, but this will be necessary in light of the SOFR Surge Event. As LIBOR risk factors are a necessity and common practice in the debt capital markets (i.e., for bonds and other securities), these risk factors will need to evolve to take account of the additional risks relating to the SOFR Surge Event.

A significant difficulty with any contemplated transition from LIBOR to SOFR is that insufficient time has been given to market participants to observe how LIBOR and SOFR compare over a period that includes time to capture events such as the SOFR Surge Event, as well as more significant market events, such as downturns in the economic cycle, periods of heightened sovereign risk, periods of significant change to asset prices or major global conflicts. As a result, the risk exists that neither financial institutions nor customers will be able to readily develop sophisticated hedging products that allow the differences between SOFR and LIBOR to be effectively and cost efficiently managed.

All this raises questions as to whether the markets and the regulators have sufficiently thought through the appropriateness and benefits of adopting SOFR in place of LIBOR as the leading USD floating rate benchmark and the risks it poses to the cash and derivatives markets, and long term debt capital markets, as a fall back for LIBOR.

[1] See Douglas Adams, Hitchhiker's Guide to the Galaxy, on encountering tea from a Nutri-Matic machine.