Jump to...

Cabinet resolution number 31 of 2019 concerning economic substance requirements was recently published on the Ministry of Finance website. The issuance of this resolution requires companies operating a ‘relevant activity’ in the UAE, including those operating in financial free zones (such as the DIFC and ADGM), to satisfy certain substance and reporting requirements. The consequences of non-compliance include financial penalties, disclosure of the company’s information to foreign regulators and, in case of persistent non-compliance, the possibility of suspending or withdrawing the trade license of the company. ‘Relevant activities’ include activities of holding companies.

In response to the work undertaken by the European Union (EU) Code of Conduct Group[1] and the Organisation for Economic Cooperation and Development[2] relating to the imposition of substantial activity requirements for certain zero or low tax jurisdictions, the United Arab Emirates (the UAE) on 30 April 2019 issued the Cabinet of Ministers Resolution No. 31 of 2019 concerning economic substance regulations (the “Resolution”), effective from 30 April 2019 (the “Effective Date”).

The UAE has introduced the required measures in order to prevent the jurisdiction from being included on the EU’s ‘blacklist’ of non-cooperative jurisdictions. The EU dictates a number of criteria for non-cooperative jurisdictions to comply with in order to be removed from the blacklist, including not facilitating offshore structures or arrangements aimed at attracting profits which do not reflect real economic activity in the jurisdiction (more commonly referred to as ‘criterion 2.2’). The Resolution is broadly in line with the EU criteria. Aside from this, the implementation of the Resolution should further benefit the UAE in helping to address various reputational concerns e.g., in respect of transparency, which the jurisdiction has been subject to from international players and investors alike.

The Resolution has been anticipated for some time after a number of other zero or low tax jurisdictions, including the Bahamas, Bahrain, Bermuda, the British Virgin Islands, the Cayman Islands, Guernsey, the Isle of Man and Jersey implemented economic substance legislation on 1 January 2019. However, whether the Resolution goes far enough to satisfy the EU’s requirements and ultimately facilitate the UAE’s removal from the EU’s blacklist still remains to be seen.

The Resolution applies to all UAE onshore and free zone companies (including branches and representative offices) which undertake the following activities (the “Relevant Activities”):

The Resolution expressly excludes any entities which are directly or indirectly owned by the UAE government (both federal and local), or any governmental authority or body. This means that UAE sovereign wealth funds and their related group subsidiaries are exempt, but free zone-incorporated holding companies within non-sovereign groups, such as those commonly established in the ADGM or DIFC, will fall within the scope of the Resolution.

In order to satisfy the economic substance requirements under the Resolution, any corporates which undertake Relevant Activities are required to:

It is worth noting that holding companies benefit from less stringent requirements (see section 3 below), whilst entities carrying out ‘high risk’ IP-related activities will be subject to additional requirements to those listed above.

The Resolution states that further guidance will be issued to assist companies in their compliance with the economic substance requirements, which will also include guidance around the interpretation of terms such as ‘adequate’. In any event, it is unlikely that the interpretation of such terms is intended to be prescriptive, and what is deemed to be ‘adequate’ will vary in accordance with the facts and circumstances of the company and Relevant Activity in question.

The Resolution also provides that companies will be able to appoint third-party service providers to fulfil certain of their economic substance requirements, but in doing so, the company must be able to show that it has full control over the activity designated to the third party and that the service provider has, in its own right, an adequate presence in the UAE.

Based on our reading of the Resolution, a holding company is defined as an entity which generates income purely from capital gains and receipt of dividends. Under the Resolution, such holding companies will be not be required to meet the economic substance requirements through the general economic substance test, as set out in section 2 above, but instead meet the economic substance requirements through the following.

i. Satisfaction of all reporting requirements under its regulating law; and

ii. Maintenance of sufficient premises and employees to carry out its activities.

Clearly, what is sufficient in the context of a holding company will be a much lower test than an entity purporting to undertake an income-generating business activity, whereby a registered office and director/employee engaged for the purposes of filing and reporting should arguably be sufficient.

However, it should also be noted that holding companies generating income from activities other than capital gains and receipt of dividends may not be classed as holding companies for the purposes of the Resolution, and consequently will likely be held to the higher standard of economic substance due to their carrying out of such activities. Therefore, non-sovereign groups will need to maintain strict procedures to prevent other income streams from feeding into their holding company structures.

Nominee Structure Background

The maximum permitted shareholding by a foreign business in a UAE ‘onshore’ entity is 49%, with the remaining 51% having to be held by a local partner. In order to retain as much de facto control as possible over the ‘onshore’ entity, foreign investors often put in place a private contractual arrangement underpinning the 49:51 investment structure, which generally provides foreign investors with additional controls through, for example:

ADGM/DIFC Trust Structure Background

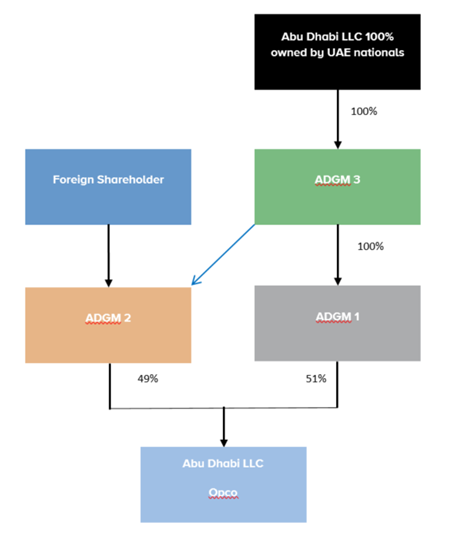

A more commonly used structure to the nominee arrangement is a holding company trust structure, which is typically put in place by a foreign shareholder under the laws of the ADGM or DIFC in order to satisfy UAE foreign ownership requirements, and manage and structure its shareholding in a UAE ‘onshore’ entity with a local partner as efficiently as possible. Albeit more complex to put in place, this structure is generally preferred to a nominee arrangement as it provides greater certainty and control to foreign shareholders.

A typical example of an ADGM trust structure (also applicable in the DIFC) would involve the following steps:

i. The incorporation of a number of ADGM companies, which acquire the majority of shares in the ultimate UAE ‘onshore’ company.

ii. One ADGM company becomes the immediate holder of the ‘onshore’ company’s shares, and the shares in that ADGM company thereafter become the ‘trust assets’ held by another ADGM company operating as trustee under a trust. The local partner holds the shares in the trustee.

iii. The trust itself is not a legal entity but is created under equity (a common law doctrine recognised by ADGM and DIFC law) which establishes an extra-contractual obligation on the trustee to hold the trust assets for and on behalf of a named beneficiary (i.e., the foreign shareholder).

iv. Under the applicable trust law, whether in the DIFC or the ADGM, the trustee has equitable obligations in relation to the holding of the assets and holds the legal title to the trust assets solely to give effect to the trust arrangement.

Please see the example trust structure diagram in the Annex for reference.

Impact of Resolution

We do not expect nominee arrangements or ADGM/DIFC trust structures to be impacted materially by the Resolution, provided that the entities used in such structures do not derive income from other sources.

Simply entering into a nominee arrangement/trust agreement for no consideration (as is possible under a deed of trust) should mean that a holding company does not derive any income, from acting as a trustee or otherwise. Similarly, the nominee beneficiary/beneficiary of a trust should only receive distributions or capital transfers relating to the subject of the nominee arrangement/trust, both of which should therefore fall within the permitted income streams in the Resolution. This analysis should be revisited, however, where fees are payable to entities within the group that seek to act just as holding companies.

Conversely, caution should be taken in a situation where a nominee beneficiary has provided a loan to its local partner to facilitate its acquisition of the >51% stake in a nominee arrangement, as the repayment of such loan would qualify as income from another source which would cause the nominee holding structure to fall foul of the Resolution.

We further understand that the ADGM and the DIFC are considering the issuance of additional guidelines for the licensing requirements and other implementation considerations, each with respect to companies established within its boundaries.

Please note that the contents of this section are based on our reading of the Resolution, but are subject to the tax advisers’ views on the ramifications of the issuance of the Resolution (e.g., what would be the consequences, from a tax perspective, of an entity not meeting the economic substance requirements; how to mitigate the risk of any company constituting part of the holding structure losing its UAE tax-residency status, etc.). Parties employing such structures will also have to take note of the reporting requirements, outlined below.

Reporting Requirements

The Resolution requires a company that is carrying on a Relevant Activity to prepare and submit to the authority delegated to regulate a Relevant Activity, on an annual basis following the last day of the end of each financial year, a report which shall be submitted to the UAE Ministry of Finance.

The report must be in the form approved by the UAE Ministry of Finance and shall include information, as set out under the Resolution; noting that additional information shall be required for companies with a ‘high risk’ intellectual property business or in the case where a Relevant Activity is outsourced. If the company’s records are not submitted in English, the regulatory authority may request that these are translated.

It should be noted that first reports will be due from 2020, as follows:

i. Entities possessing an existing trade licence on or before the Effective Date, must comply with the Resolution from the Effective Date onwards.

ii. Entities that received a trade licence on or after the Effective Date must comply with the Resolution only from the date the trade licence was received.

Penalties

Non-compliance with the Resolution may result in hefty administrative penalties being imposed as well as possible deregistration. Penalties shall apply in the case where the economic substance test is not met and where the company failed to provide required information or has provided information which is inaccurate. In both instances, an administrative fine of not less than AED10,000 and not more than AED50,000 shall be imposed. Furthermore, a penalty of not less than AED50,000 and not more than AED300,000 shall be imposed in the subsequent financial periods for repeated non-compliance, subject to a six year limitation period.

In addition to the aforementioned penalties, the regulatory authority may decide to suspend, revoke or deny renewal of a company’s license. The Ministry of Finance also has the authority to report any non-compliance to a company’s foreign regulators, which could attract strong and unwanted scrutiny.

Generally speaking, the Resolution should have a limited impact on companies that have an income-generating presence in the UAE, and undertake genuine business activities on the ground. Income-generating entities which are managed remotely should be reassessed in light of the Resolution.

Holding companies, including nominee and/or ADGM/DIFC trust structures, must be clear on the sources of all income coming into such holding structures, in order to not fall foul of the Resolution. We recommend that businesses with a nominee or ADGM/DIFC holding company review any such structures carefully in light of the Resolution, and further begin to bring annual reporting in line with the new requirements.

Notes to diagram:

[1] Scoping Paper issued on 22 June 2018

[2] Guidance published on 15 November 2018 on the application of the substantial activities factor to no or only nominal tax jurisdictions

Partner

Industries

Regional Experience