November 27, 2020

Jump to...

On October 27, 2020 the U.K. Takeover Panel (the “Panel”) published a consultation (the “Consultation”) on a series of significant changes to the treatment of conditions (and pre-conditions) to offers and the timetable which offers must follow under the U.K. Takeover Code (the “Code”). The consultation calls for comments by January 15, 2021, following which the Panel expects to issue a response statement (in Spring 2021) setting out the final form of the changes it decides to make to the Code.

The changes to the Code include:

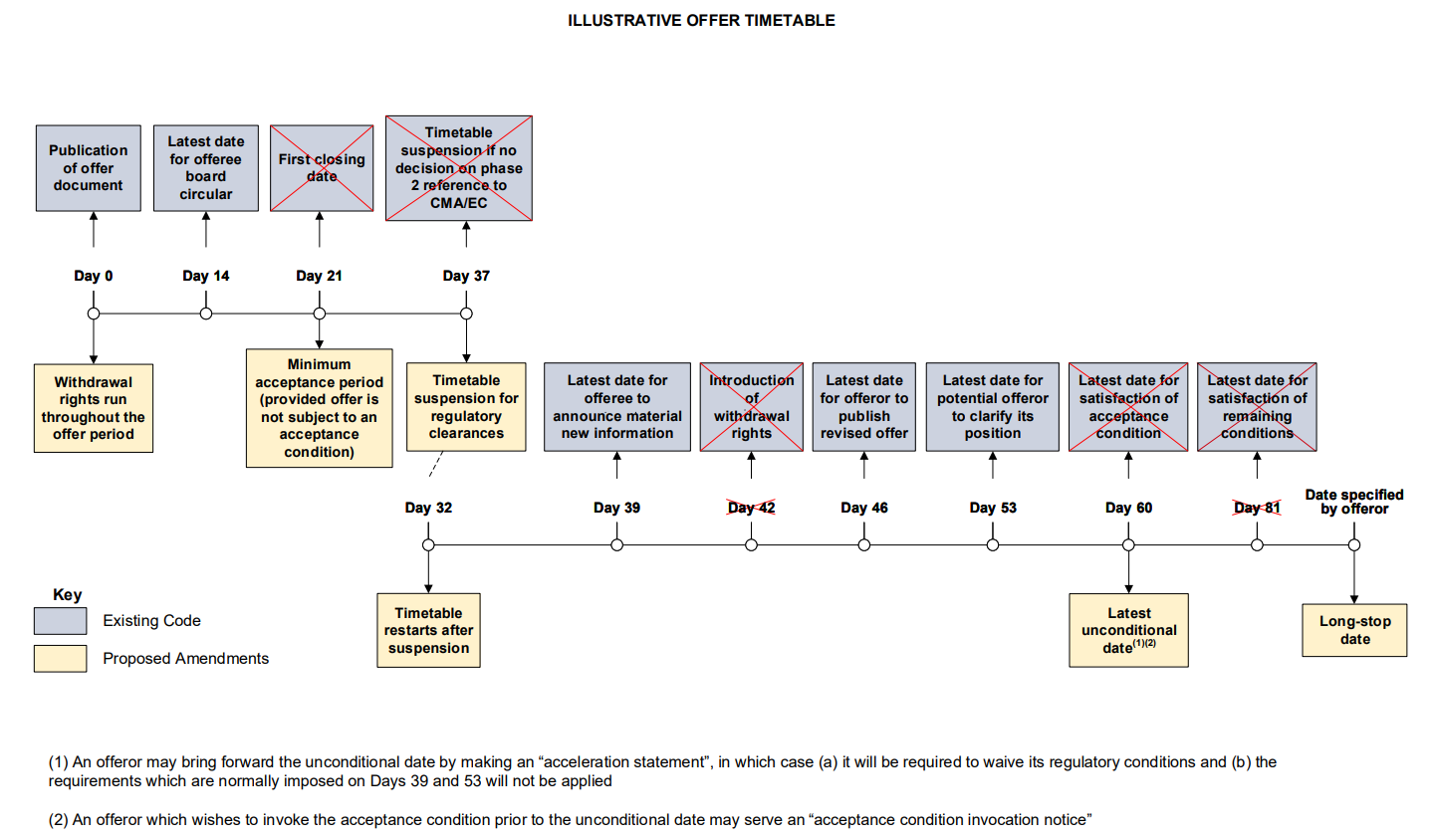

The illustrative timetable set out below is taken from the Consultation and provides a summary of some of the key proposed changes to the Code’s offer timetable for contractual offers. These changes will not apply to offers implemented by a scheme of arrangement which will continue to be governed by their own scheme timetables complying with the requirements for schemes in Appendix 7 to the Code.

The timetable changes are largely focused on simplifying the Code’s timetable and updating it to take account of the pressures created by the increasingly common and potentially lengthy multiplicity of official authorizations and regulatory clearances (“Regulatory Approvals”) to which many offers are now subject. These approvals extend well beyond the Phase 2 References which the Code has historically and specifically addressed.

The timetable changes—which while significant are not thought likely to lead to any big changes in the way in which bids are structured or play out once launched—include the following.

Long-stop Date: bidders will be required to include in their offers a long-stop date which will be the date by which, if there has been a delay in the offer becoming unconditional on the Unconditional Date (see below) (e.g. because of a suspension of the offer timetable (see “Suspending the Code Timetable” below)), the offer will lapse, subject as mentioned below.

This requirement will also apply to pre-conditional offers and be the date by which all pre-conditions must have been satisfied or waived for the bidder to proceed with its firm offer.

If the relevant conditions or pre-conditions are not satisfied or waived, whether the bidder can lapse its offer will depend on whether the unsatisfied condition is:

For recommended offers the Long-stop Date can be agreed (and extended) between bidder and target. For hostile (or unilateral) offers the Panel will: (i) have to be consulted (and consent to any extension of the date), and (ii) require the date to be no earlier than the date by which the bidder reasonably expects the condition (or pre-condition) relating to the “slowest” Material Regulatory Approval to be satisfied.

Day 81: (counting from the date of publication of the offer document) currently this is the latest date by which, following satisfaction of the acceptance condition on Day 60, all conditions to the offer must be satisfied or waived, failing which the offer will lapse. As discussed below, this date will no longer feature in the offer timetable.

Day 60: at present this is the deadline by which the bidder’s acceptance condition must have been satisfied. This will now become the date by which all conditions to the offer must have been satisfied. There will no longer be a distinction between an offer becoming unconditional as to acceptances and all other outstanding conditions having to be satisfied within 21 days thereafter. The acceptance condition will no longer be capable of being satisfied until all other conditions are satisfied. Target shareholders will no longer therefore be in the position, as they are under the existing Code rules, of being locked into their acceptances following the offer having become unconditional as to acceptances while the offer remains conditional on the satisfaction of other conditions, for a possible further 21 days (or even longer if the Panel exceptionally grants an extension to Day 81).

The Panel may consent to an extension to Day 60 in certain defined circumstances and the Consultation proposes that these should include delays in obtaining a Material Regulatory Approval (instead of, as at present, a significant delay in a decision as to whether there will be a Phase 2 Reference) (see “Suspending the Code Timetable—Proposed equal treatment of all Material Regulatory Approvals for timetable suspensions” below).

Unconditional Date: a new definition in the Code, this would be when all conditions must be satisfied or waived. It will be Day 60 unless the bidder has brought it forward by making an Acceleration Statement (see below) or, following consultation with the Panel, the bidder specifies an earlier date in its offer document.

Days 53/46/39: these dates will remain, as they currently are, the latest dates by which: (i) another identified potential competing bidder must “put up or shut up,” (ii) the bidder can revise its offer, and (iii) the target can release any material new information, respectively, but will be set by counting back from Day 60 so that they automatically move with any extension of Day 60 following the timetable’s suspension.

Day 42: currently the date when withdrawal rights become exercisable by target shareholders who have accepted the offer (i.e. 21 days after the typical first closing date (which cannot be earlier than 21 days after the offer document is published)); this date will cease to have relevance since withdrawal rights will now be exercisable as from the offer document being published (see “Withdrawal Rights and other proposed changes to the Code” below).

Day 32: this will be a new date in the Code timetable and will normally be the date when an offer resumes following satisfaction or waiver of a Material Regulatory Approval condition (see “Suspending the Code Timetable—Ending the timetable suspension” below).

Day 21: currently the first permitted closing date for offers, this will become the minimum period for which an offer must be open for acceptance. “Closing dates” will no longer feature in the Code timetable. If a bidder wishes to close its offer before Day 60 it could issue either an Acceleration Statement bringing forward the Unconditional Date for its offer or, as appropriate, an Acceptance Condition Invocation Notice (see below).

Day 14: will remain as the latest date by which the target can respond to the bidder’s offer document.

Acceleration Statements

As noted above a bidder will be able to bring forward the Unconditional Date for its offer by making an Acceleration Statement. This will broadly have the effect of a “no extension statement” issued under the existing Code rules. The Consultation notes that this would likely be an option for a bidder which wanted its offer to succeed.

The statement would have to fix a new Unconditional Date not less than 14 days from when it is made and must waive all unsatisfied Regulatory Approvals. The bidder will not be permitted to set the statement aside except where, after consultation with the Panel, it has specifically reserved the right to do that or in “wholly exceptional circumstances.” If the bidder wishes to fix an Unconditional Date in its offer document earlier than Day 60, it will normally be treated as having made an Acceleration Statement and must consult the Panel in advance.

Where an Acceleration Statement is made, the Day 53 and Day 39 rules (see above) will not apply.

Acceptance Condition Invocation Notices (“ACINs”)

The Consultation proposes that a bidder, which wishes to lapse its offer prior to the Unconditional Date, may issue an ACIN under which the date for satisfaction of the acceptance condition would be brought forward to a specified date no earlier than 14 days after the date of the notice. The ACIN would be irrevocable and if the bidder wishes to “waive down” the level of acceptances required, this would have to be done in the ACIN and not after the ACIN had been issued. If the required level of acceptances was not reached on the specified date, the offer would lapse but if that level was reached the acceptance condition would only be treated as satisfied if and when all other conditions were satisfied or waived.

Announcement of Acceptance Levels

Currently, a bidder is only required to announce the level of acceptances for its bid on the business day following the day on which its bid is due to expire (i.e. on a closing date), when it becomes unconditional as to acceptances or when it is revised or extended. The Consultation proposes that the bidder make these announcements much more frequently: (i) on Day 21 and every seventh day thereafter, (ii) each of the five business days up to and including the Unconditional Date, (iii) whenever an ACIN expires or the offer lapses or is declared unconditional, and (iv) on any day when the level of acceptances passes through certain thresholds (the current stated acceptance level, the minimum acceptance level and 75% of the voting rights in the target).

Suspending the Code Timetable

Special Treatment of Phase 2 References Under the Existing Code

Currently, Phase 2 References are, for historical reasons, afforded special treatment under the Code, in that: (i) an offer will automatically lapse if there is a Phase 2 Reference, (ii) an extension of the timetable will be permitted (without the need for the target’s agreement) where there is a delay in the decision whether there will be a Phase 2 Reference, (iii) Panel consent is not required for the inclusion of a Phase 2 Reference as a pre-condition, and (iv) a Phase 2 Reference condition (or pre-condition) is not subject to the Code’s restrictions on invoking conditions so as to cause an offer to lapse. This treatment is not available to other Regulatory Approval conditions unless, in a particular case, the Panel can be persuaded to give its consent.

With regards to extensions of the Code timetable (i.e. Day 60) to accommodate delays in obtaining other Regulatory Approvals, if the target will not consent, the bidder will be forced to ask the Panel for an extension to Day 81 which will only be granted in the case of a Material Regulatory Approval. However, the Panel is usually reluctant to agree such an extension because it will result in accepting shareholders remaining locked into the offer, unable to exercise withdrawal rights following satisfaction of the acceptance condition on Day 60 and forced to wait until resolution of the issue before receiving their offer consideration.

Proposed Equal Treatment of All Material Regulatory Approvals for Timetable Suspensions

The Consultation proposes removing the special treatment of Phase 2 References mentioned above. An offer will no longer automatically lapse if there is a Phase 2 Reference and Phase 2 References would in future be treated in the same way as any other Regulatory Approval as regards pre-conditions and conditions (see “Conditions and Pre-conditions—Proposed equal treatment of all Regulatory Approvals as pre-conditions or conditions” below).

With regards to extensions to the Code timetable, a new rule would be introduced under which the Panel will normally suspend the Code timetable if, by 5 pm on the second day prior to Day 39, a Regulatory Approval remains outstanding and either: (i) both bidder and target request this, or (ii) one of them requests this and the Regulatory Approval is a Material Regulatory Approval. The Consultation states that the Panel should normally only consent to a suspension after this deadline if the target agrees or in exceptional circumstances (e.g. where in the later stages of the offer a regulator determines for the first time and contrary to the expectations of the parties that a Material Regulatory Approval is required).

The Panel acknowledges that this new suspension right could in future put targets under “bid siege” for a longer period, but argues that targets have always been vulnerable to the protracted siege of a pre-conditional offer.

Ending the Timetable Suspension

Where the timetable suspension ends, the timetable will resume on Day 32. The suspension will end: (i) when the relevant Regulatory Approval is obtained or waived, or (ii) the parties agree it should end, or (iii) if the bidder makes an Acceleration Statement in which it waives all outstanding Regulatory Approval conditions and sets a new Unconditional Date of not less than 14 days (and not more than 27 days) from the date of the Acceleration Statement.

Suspensions in the Case of Competing Offers

When a suspension of the timetable is requested by one of two or more competing bidders or the target, the timetable will normally be suspended for all the bidders and will only be resumed by the satisfaction or waiver of the latest bidder’s Material Regulatory Approval condition or by the target agreeing with the bidder that the suspension should end. A bidder who wished to resume its bid while the suspension continued for other bidders would be able to make an Acceleration Statement to reintroduce into its bid timetable an earlier Unconditional Date.Since a bidder would not be required to extend its Long-stop Date to align with that of a competing bidder, if the suspension remained in force at its Long-stop Date the bidder would have to decide whether to waive the relevant condition Material Regulatory Approval or seek the Panel’s agreement to invoking the condition to lapse its bid by reference to the continuing material significance of the condition at that time.

Existing Treatment of Regulatory Approvals as Pre-Conditions or Conditions

While the Code allows a bidder making a “pre-conditional offer” (i.e. announcing a bid that will only be made if certain conditions (typically Regulatory Approvals) are obtained or waived) to include as a pre-condition a Phase 2 Reference, any other Regulatory Approval can only be included as a pre-condition if the offer is publicly recommended by the target or “the Panel is satisfied that it is likely to prove impossible to obtain the [Regulatory Approval] within the Code timetable.” In addition, while the Code prevents the bidder from invoking any condition (other than the acceptance condition) or pre-condition to cause its offer to lapse or not proceed “unless the circumstances that give rise to the right to invoke the condition or pre-condition are of material significance to the offeror in the context of the offer,” this material significance test does not apply to a Phase 2 Reference condition or pre-condition.

Proposed Equal Treatment of All Regulatory Approvals as Pre-Conditions or Conditions

This special treatment of Phase 2 References under the Code would be replaced by identical treatment for all Regulatory Approvals. Thus:

Reassessment of the Material Significance Test for Material Regulatory Approval Conditions or Pre-Conditions Before They Can Be Invoked

The Panel notes in its Consultation that the fact that it may have previously determined a condition to be a Material Regulatory Approval for the purposes of a suspension of the offer timetable or of accepting it as a pre-condition, will not stop it reassessing whether the condition or pre-condition remains of material significance to the offeror in the context of the offer when the bidder seeks the Panel’s consent to invoke the condition or pre-condition.

Revised Panel Practice Statement No. 5 (“PS 5”)

PS 5, which sets out informal advice of the Panel on the invocation of conditions (and pre-conditions), would be revised to take account of the above changes as well as to set out additional factors that the Panel would take into account when considering whether a condition or pre-condition could be invoked. These additional factors, which do not fundamentally alter the Panel’s existing approach to deciding whether a condition satisfies the material significance test for invocation, include:

Withdrawal Rights

Another very significant change proposed is that target shareholders who tender acceptances of the bidder’s offer will be able to withdraw their acceptances at any time up to satisfaction of all remaining conditions by the Unconditional Date (or earlier if the bidder has issued an Acceleration Statement to bring that date forward (see “Offer Timetable—Acceleration Statements” above)). At present, in the normal course, acceptances can only be withdrawn as from (typically) Day 42 (see “Offer Timetable” above). This restriction already does not apply to offers subject to U.S. securities laws owing to the U.S. base of target shareholders and will now be removed altogether. This will not affect target shareholders continuing voluntarily to give up their withdrawal rights by entering into irrevocable commitments which preclude them from doing that.

Schemes

Another proposed change will require bidders to take any necessary procedural steps required from their end in order for a scheme that implements an offer to become effective. These steps include confirming to the court that all the other offer conditions have been satisfied and undertaking to the court to be bound by the scheme as it applies to the bidder. The bidder will usually agree to take these steps in its bid conduct agreement with the target, but the Code would now impose this requirement directly on the bidder. This would prevent a bidder who wished to see its offer lapse refusing to waive “immaterial conditions” that it would not be permitted by the Panel to invoke or refusing to give the required undertakings to the court, that would otherwise be required in order for the scheme to become effective by its Long-stop Date.

Mandatory Offers

The Code prohibits a bidder triggering the mandatory offer requirement if the making of the offer may be dependent on any condition or consent. The only condition to which such offers should be subject is a minimum 50%+1 acceptance condition. However, the Panel will, in exceptional circumstances, consider disapplying this prohibition, including when a Regulatory Approval is required before the bidder’s offer document can be published. In that case, the document must be published immediately if the Regulatory Approval is obtained, but where it is not, the Panel will require the bidder to reduce its interest in the target to below the mandatory bid threshold (i.e. 30%).

The Panel is proposing that the prohibition would only be disapplied if the share purchase agreement for the acquisition which triggers the mandatory bid is made subject to a condition in identical terms to the Material Regulatory Approval condition (or pre-condition) in the mandatory bid. The bidder will only be permitted to invoke that condition in the share purchase agreement with the consent of the Panel (which will only be given where it would normally be given by the Panel for the invoking of any condition in an offer, i.e. where the material significance test is met). No other conditions, other than the minimum acceptance condition, would be allowed. The result will be that no acquisition triggering a mandatory bid will take place if the condition is not satisfied and so no bid will be required. If the condition is satisfied, the bid must be made. In addition, immediately on the share purchase agreement being entered into, the bidder will have to make a firm offer rule 2.7 announcement.

Final form changes to the Code are expected to come into force before the second half of 2021, three months after the Panel’s issue of a Response Statement to comments on the proposed changes. This delay will allow practitioners and others time to familiarize themselves with the revised Code which will apply to firm offers announced after that time.

Practices

Regional Experience